• Other mega forces are driving returns beyond AI. This keeps us overweight Japanese stocks, while we favor pharmaceuticals and financials in Europe.

• The U.S. Supreme Court struck down the use of emergency powers to impose tariffs. The administration is already taking other measures to reimpose them.

• Final euro area inflation data is in focus this week after the ECB held rates steady. We see policy rates on hold through 2026 if inflation slips below 2%.

Markets are laser-focused on the AI buildout, but opportunities shaped by other mega forces abound. Case in point: Japan and Europe are ramping up fiscal spending to boost self-sufficiency amid geopolitical fragmentation. Fiscal expansion is just one reason to gain exposure to this evolving trend. In Japan, sustained corporate reforms underpin our overweight to equities. In Europe, we focus on equity sectors, favoring infrastructure, pharma and financials.

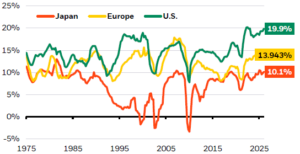

Japan’s regime shift Return on equity, 1975-2026

Source: BlackRock Investment Institute with data from LSEG Datastream, February 2026. Implied aggregate return on equity derived from index valuation ratios based on MSCI country equity indices.

International developed market stocks are outperforming this year, after walloping U.S. counterparts last year. Is it too late to jump in? We don’t think so. Japan’s return on equity (ROE) has steadily moved higher, narrowing the gap with the U.S. and Europe. See the chart. This is not just a sugar rush from fiscal expansion. It’s very much a slow-burn, structural force: A focus on capital discipline and shareholder returns is lifting underlying profitability. Japanese companies are now focused on maximizing profits, rather than minimizing debt. And a steady decline in corporate cross-shareholdings is making Japan more attractive for foreign investors. In Europe, we think overall ROEs will need to improve via productivity gains – rather than being juiced by one-off cyclical boosts. We’re focused on sectoral opportunities in the region as a result.

Japan’s corporate improvements are taking shape against a benign macro backdrop of strong nominal growth plus fiscal spending. Wages are rising, and the end of deflation has allowed companies to raise prices without losing demand. We see the historic election win for Prime Minister’s Sanae Takaichi’s Liberal Democratic Party offering continuity and predictability on this front. The LDP’s majority supports increased fiscal spending on the economy and national security. That fiscal trajectory sits within the geopolitical fragmentation mega force: it’s pushing economies toward capacity building, as nations try to become more self-sufficient. This broadening shift was on display at the recent Munich Security Conference.

In Europe, we like sectors that benefit from this increased spending on defense, infrastructure and energy, as we outlined in “What’s needed for Europe’s investment renaissance.” We see sectoral dispersion driving performance. Pharma is a prime example: the segment has solid earnings, low valuations relative to history and growth prospects thanks to AI innovation and a rapidly greying population. Financials are another top pick. Europeans are big savers and policymakers are making it easier for households to invest – a shift also underway in Japan via the Nippon Individual Savings Account (NISA) program – and for companies to raise capital through initiatives such as the EU’s Savings and Investment Union (SIU). We see undervalued European financials poised to channel these savings into productive investment.

The key risk: fiscal expansion does not come for free in bond markets. Investors are scrutinizing debt sustainability and demanding more compensation to hold long-duration paper as governments raise strategic spending. That shows up as higher term premia and upward pressure on long-end yields, most visibly in Japan but increasingly relevant elsewhere. Beyond this, higher issuance and stickier inflation can keep long rates elevated. That is why we stay underweight government bonds, particularly at the long end, relative to equities.

Bottom line: Fiscal expansion tied to geopolitical fragmentation is creating return drivers outside of AI. We prefer Japanese equities over government bonds on a combo of corporate reforms and fiscal support. In Europe, we see sector dispersion driving outcomes. We focus on stimulus beneficiaries such as infrastructure, as well as pharma and financials.